Currently it is common nationally and internationally to portray all lawyers as ‘enablers’ of crime. The Council of Bars and Law Societies of Europe (CCBE) in its newsletter of October/November objected to that qualification:

However, the CCBE strongly opposes the generic categorisation of lawyers as “enablers”. Lawyers are genuinely “gatekeepers”, not “enablers”. As underlined by the Organisation for Economic Co-operation and Development (OECD), “The majority of professionals are law-abiding and play an important role in assisting businesses and individuals to understand and comply with the law and helping the financial system run smoothly. Such law-abiding professionals are to be differentiated from a small set of professionals who use their skills and knowledge of the law to actively promote, market and facilitate the commission of crimes by their clients”.

Unfortunately, this will not stop the incorrect framing by certain journalists, politicians and bankers.

European consultation on ‘enablers’

This position was taken by CCBE in an article on its participation the European Commission consultation on “Tax evasion & aggressive tax planning in the EU – tackling the role of enablers”. CCBE presented its response (pdf) to that consultation.

The questionnaire itself is already interesting, it shows the biases of the European authors in regard of ‘the enabler’ and it shows binary thinking, in terms of black/white & good/bad. The questionnaire even contains a question on a ‘register of enablers’, a horrifying idea.

It is courageous of CCBE to reply in an independent and thorough way, probably knowing that the answers are politically undesirable and will be ignored.

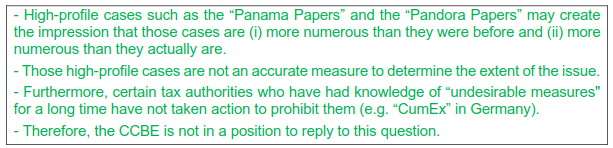

CCBE doesn’t agree with the much repeated assertion that tax evasion and agressive tax planning “continue to be a substantial problem in the European Union” (3.1), they answer they do not know and explain:

The assertion that there is an increase in tax evasion or aggressive tax planning (3.3) gets the same answer and this explanation:

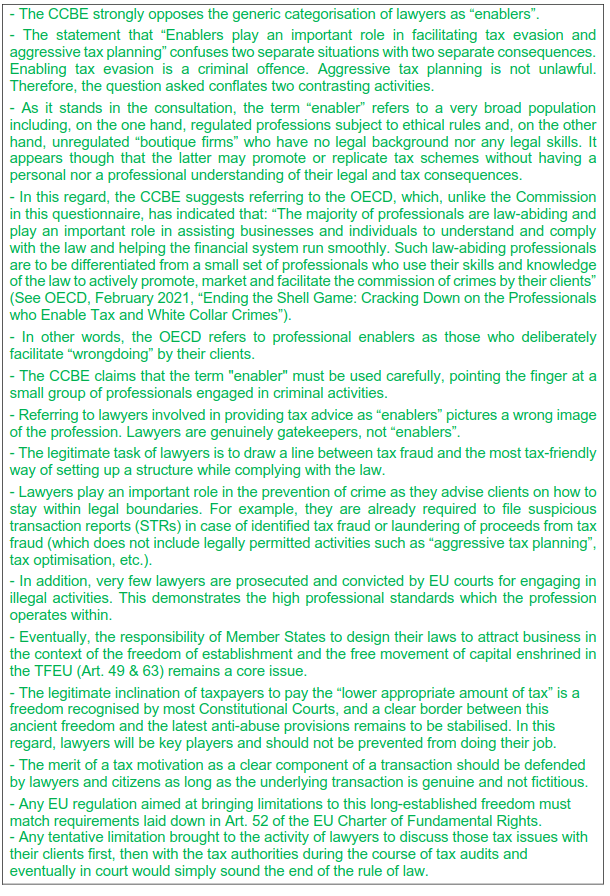

CBBE disagrees with the assertion that enablers play an important role in facilitating tax evasion and aggressive tax planning (3.5):

Read also the other questions and answers. It provides useful information about European thinking and raises concerns for the future of the legal profession. The same type of European thinking underlies the AML Package, from which little good can be expected.

Read also my article European report on tax intermediairies | facilitators, tax compliance.